Following today's retail sales and industrial production reports, the Atlanta Fed's GDPNow tracking model revised real GDP growth down to -1.5% (saar) during Q2 from -1.2%. Real consumption spending was lowered from 1.9% to 1.5%, while gross private investment now shows a decline of -13.8% instead of -13.7%. Consider the following:

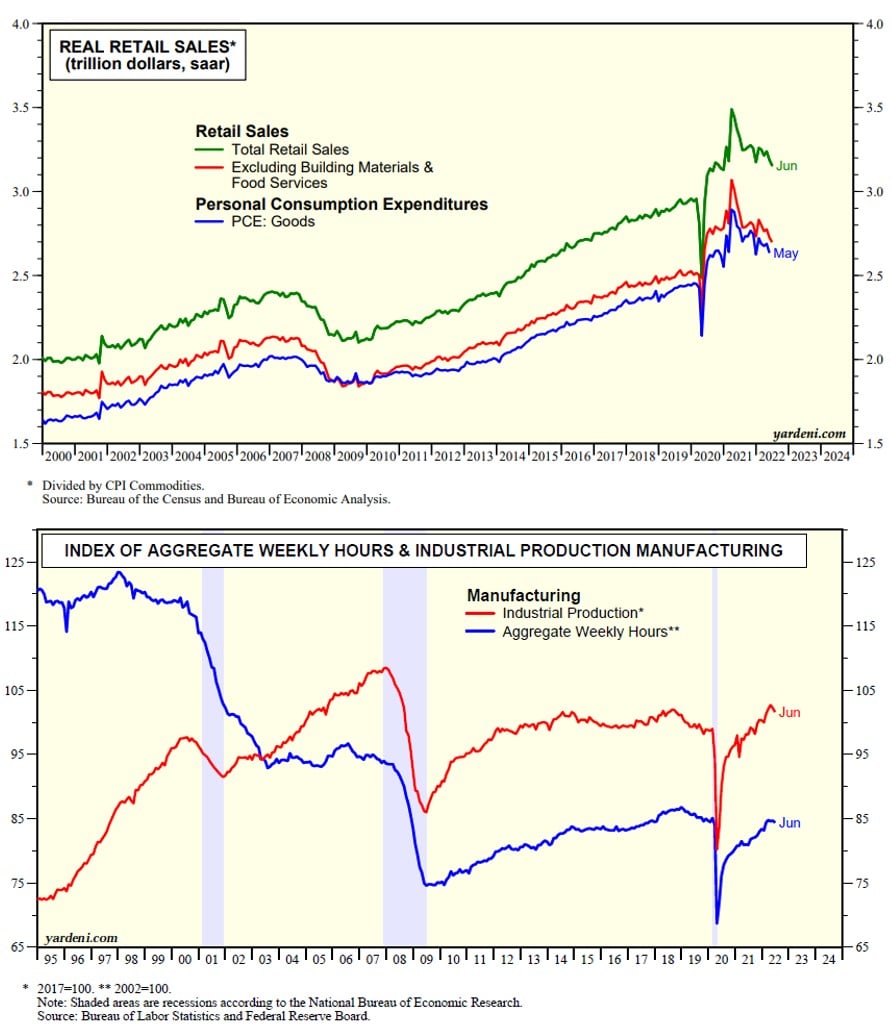

(1) Retail sales. Adjusted for inflation, retail sales has been mostly falling over the past year, and did so again in June (chart below). Consumers satiated lots of their pent-up demand for goods, and then some, following the lockdowns in early 2020. To relieve their cabin fever they went on a buying binge, but were limited mostly to purchasing goods since the availability of many services remained limited. In recent months, consumers have pivoted to purchasing services. Some of them, of course, have had to spend a larger share of their budgets on essentials such as food, fuel, and rent, forcing them to reduce their discretionary purchases of both goods and services. Department store sales and housing-related sales both declined in June.

(2) Production. Industrial production edged down -0.2% m/m in June led by a second consecutive monthly decline of -0.5% in manufacturing output (chart below). The weakness was widespread. Motor vehicle assemblies edged down in June. So did housing-related output of construction supplies as well as appliances, furniture, and carpeting. Also down were production in the aerospace and defense industry as well has high-tech industries. Energy output has been a standout, rising in recent months.

(3) Bottom line. Both retail sales and industrial production are coincident economic indicators. They point to slower economic growth. However, payroll employment is also a coincident indicator, and it was strong in June. It all adds up to a growth recession, a.k.a., a mid-cycle slowdown.